Retirement planning isn’t just about saving—it’s about making your money last. With nearly half of retirees fearing they’ll outlive their savings, using the right strategies is essential.

This article breaks down the six key steps to stretch your retirement funds, from using flexible withdrawal strategies to smart tax planning, keep reading to learn how to avoid running out of money in retirement.

By: William Hinder, EA | February 15th, 2025

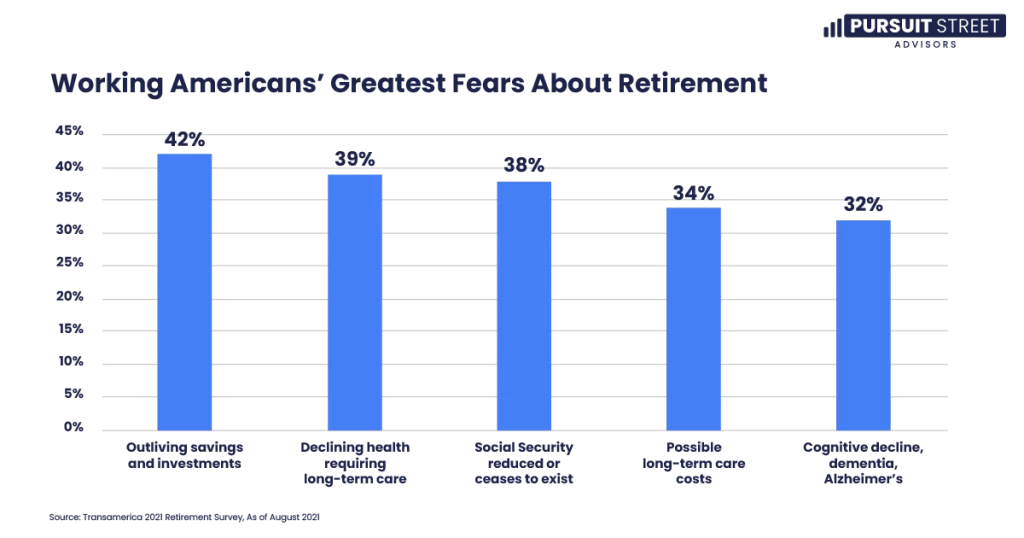

One of the biggest fears in retirement planning is making sure your retirement savings last.

After years of hard work, financial stability should not be a lingering worry. But over 48% of retirees say outliving their savings is their biggest fear, even more so than dementia or Alzheimer’s!

With rising living costs, market fluctuations, and unexpected expenses, managing retirement funds wisely is essential.

The key to a financially secure retirement lies in smart planning, disciplined withdrawals, and the flexibility to adapt to life’s changes. By leveraging tax-efficient strategies and diversifying investments, you can build a rock-solid plan that keeps your money working for you.

A secure retirement starts with proper retirement planning long before leaving the workforce.

If your savings are not where they should be, postponing retirement can help ensure a more stable financial future.

Like I mentioned in my article called “When Can I Retire?”, its not about your age, but your preparedness!

Maximizing contributions to retirement accounts, such as 401(k)s and IRAs, provides a solid foundation. Taking full advantage of employer matching contributions and tax-advantaged accounts can significantly boost retirement savings.

Reducing unnecessary spending during peak earning years frees up more funds for investment, compounding growth over time.

For those of you who find themselves behind on their savings goals, extending working years allows investments more time to grow before drawing them down. Working longer also enhances Social Security benefits in two major ways.

First, since Social Security is based on the average of your 35 highest earning years, it increases your average indexed earnings for the purpose of a higher Social Security benefit.

Second, delaying Social Security during working years can also lead to higher monthly payouts later. So, as you can see, just a few additional years in the workforce can make a substantial difference in long-term financial stability.

Many retirees stick to traditional withdrawal strategies, like taking out a fixed percentage each year, but a more flexible approach can often be more effective.

While it’s a good starting point, I’m not a huge fan of the popular 4% rule, which recommends withdrawing 4% of savings annually, because it doesn’t account for YOUR individual circumstances or economic/market conditions.

What if you could afford to spend more but didn’t realize it? Or what if 4% is actually too much for your situation?

Adapting withdrawals to match personal expenses and market performance is a much better approach.

Rather than rigidly increasing your withdrawals based on inflation, you could consider a flexible strategy that allows you to withdraw less during economic downturns and more when markets perform well.

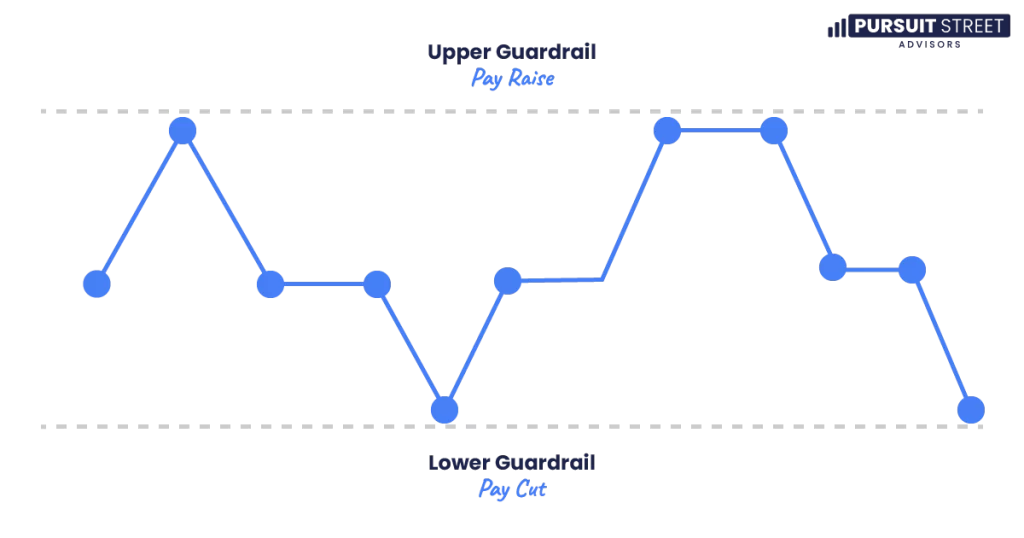

We call this the “guardrail” strategy.

Think of it like driving on a highway, where guardrails are in place to keep you from veering off course.

In this analogy, your portfolio withdrawals are the car—we want to keep it safely on track, but the guardrails act as a safety measure just in case.

If you hit the lower guardrail, meaning your portfolio has decreased in value by a certain threshold, you would reduce spending by a predetermined amount until it recovers.

On the flip side, if you hit the upper guardrail, indicating strong portfolio performance, you can increase your spending to take advantage of the gains.

Market fluctuations are inevitable, and rigid financial plans can create difficulties during downturns.

A flexible withdrawal strategy allows retirees to adjust spending based on economic conditions.

When markets decline, reducing withdrawals helps protect your investment portfolios from being depleted too quickly.

Conversely, during strong market performance, increasing withdrawals can allow you to enjoy financial gains without jeopardizing long-term security.

By staying adaptable, you can better manage various financial risks and maintain your retirement funds for the long haul.

Tax-efficient retirement strategies play a significant role in ensuring retirement funds last. Thoughtful retirement planning regarding the order of withdrawals from different accounts can help reduce tax burdens and maximize available funds.

The common, conventional wisdom says to take withdrawals as follows…

This strategy seeks to withdraw from taxable accounts first, allowing tax-deferred and tax-free accounts like traditional IRAs and Roth IRAs to continue growing.

However, if you have multiple retirement savings accounts and a relatively consistent annual income need, a more effective strategy may be proportional or, “pro-rata” withdrawals.

This approach involves determining a target withdrawal amount and then withdrawing from each account in proportion to its share of total savings. This method can help maintain a more predictable tax burden throughout retirement while potentially reducing overall lifetime taxes and increasing after-tax income.

However, for retirees with substantial long-term capital gains and who could qualify for the 0% capital-gains tax rate, it may make sense instead to withdraw from taxable accounts first.

This strategy aims to capitalize on zero, or low long-term capital gains tax rates, depending on ordinary income tax brackets. Long-term capital gains (for assets held over a year) are taxed at 0%, 15%, or 20%, based on taxable income and filing status.

By spreading out taxable income more evenly over retirement, you may also be able to reduce the taxes you pay on Social Security benefits and the premiums you pay on Medicare.

By strategically managing withdrawals, you can minimize the tax impact and preserve more of your wealth.

Additionally, tax planning for retirees, such as harvesting capital gains and using tax-loss harvesting, can further enhance savings.

Taxes must be managed one way or another, so whether you take the time to learn about the tax code yourself, or work with a financial advisor who specializes in tax planning for retirees, you cannot disregard your current and future tax liability.

Social Security benefits are a critical income source for many retirees, and maximizing these benefits requires careful planning.

While benefits can be claimed as early as age 62, delaying claims increases the payout significantly. For every year Social Security is delayed beyond full retirement age, your benefits increase by approximately 8% per year up to age 70.

Coordinating Social Security benefits with other income sources is also essential for tax efficiency. Some retirees may benefit from drawing from taxable accounts while delaying Social Security benefits to maximize future payments.

Additionally, understanding spousal and survivor benefits can provide further financial security, enhance their lifetime income and reduce the risk of running out of money.

A well-diversified investment portfolio helps balance risk and maintain financial stability. Using a structured approach, such as the “bucket strategy,” can help segment investments into different categories based on time horizon and risk tolerance.

Picture your retirement portfolio as three distinct buckets:

This strategy isn’t just about organization – it’s about peace of mind. When the market tanks (and it will), you won’t need to sell your investments at a loss because you’ll have your cash bucket to rely on!

By maintaining a diversified portfolio with assets allocated across different risk levels, you can navigate market volatility while ensuring your income isn’t disrupted.

Let’s talk about annuities. I know, I know – annuities get a bad rap. But hear me out.

The right type of annuity, purchased at the right time, can provide something invaluable: guaranteed income for life. With interest rates rising, annuities are becoming more attractive than they’ve been in years.

Think of it like a private pension plan.

For those seeking added financial security, guaranteed income options can create a steady cash flow throughout retirement.

Annuities, for example, provide lifelong income in exchange for a lump sum investment. While annuities may offer lower returns compared to stocks, they can provide peace of mind by guaranteeing a consistent income in retirement.

Staggering or laddering annuity purchases over several years can help you take advantage of varying interest rates and market conditions. While annuities are not suitable for everyone, they can be an effective tool for those looking for a reliable income stream.

Additionally, part-time work, rental income, or dividend-paying investments can serve as supplemental income sources. Exploring multiple revenue streams provides additional financial flexibility and reduces reliance on withdrawals from retirement accounts.

Here’s what I want you to take away from all these retirement planning strategies: creating a retirement that lasts isn’t about picking the perfect stock or timing the market perfectly. It’s about having comprehensive retirement investment planning that adapts to changing conditions.

These six retirement savings tips work together to help ensure you don’t run out of money before you run out of retirement. But remember – everyone’s situation is different. What works for your neighbor’s retirement portfolio management might not work for you.

Long-term financial stability starts with a solid savings foundation. Strengthening retirement savings before retirement ensures a better financial outlook and allows for a more flexible withdrawal strategy. Minimizing tax burdens through tax planning for retirees frees up more resources for living expenses. A well-balanced investment strategy helps you manage risks while ensuring continued growth.

Want to learn more about how to avoid running out of money in retirement? Ready to implement these retirement planning strategies in your own financial plan?