Every year, countless retirees hand over thousands in unnecessary taxes to Uncle Sam.

Meanwhile, their neighbors – with similar savings – pay a fraction of what they do.

I’m about to show you why – and more importantly, how to make sure you don’t leave a tip for the IRS.

Lowering taxes in retirement is not as hard as you might think, and this guide will show you exactly how in 6 easy steps.

By: William Hinder, EA | January 20th, 2025

Recently, I sat down with a successful business owner who had done everything “right.”

She’d saved diligently, building up a large balance in her traditional IRA over a 30-year career.

She was set for a comfortable retirement but had a problem: she saved too much money.

You might be wondering, how is that even possible?

Traditional IRA’s and other tax-deferred accounts have great tax advantages to encourage saving for retirement during your working years.

But here’s what most financial advisors won’t tell you: Those tax breaks you’ve been getting for contributing to your 401(k) and IRA?

They’re about to become a tax landmine in retirement.

Think of it like a loan from the government that’s about to come due at the worst possible time.

The requirement to withdraw money from a traditional IRA account once you reach a certain age is called the Required Minimum Distribution (RMD).

After age 73 you must begin withdrawing funds from traditional IRA’s and other tax-deferred retirement accounts (or age 75 if born in 1960 or later).

These Require Minimum Distributions are calculated using the balance of the tax advantaged account(s), your age, and life expectancy.

RMD’s should be calculated using the IRS Required Minimum Distribution Tables.

The more money you have saved in a traditional IRA account, the more taxes you’ll eventually have to pay.

We ran the numbers on the business owner’s RMDs and her mandatory withdrawals would force her to take out – and pay taxes on – over $80,000 annually starting at 73.

And that number would grow substantially each year, potentially pushing her into higher tax brackets when combined with her other retirement income.

Even worse, if you don’t take your RMDs, or don’t take enough, you will owe a 25% penalty on the amount not distributed!

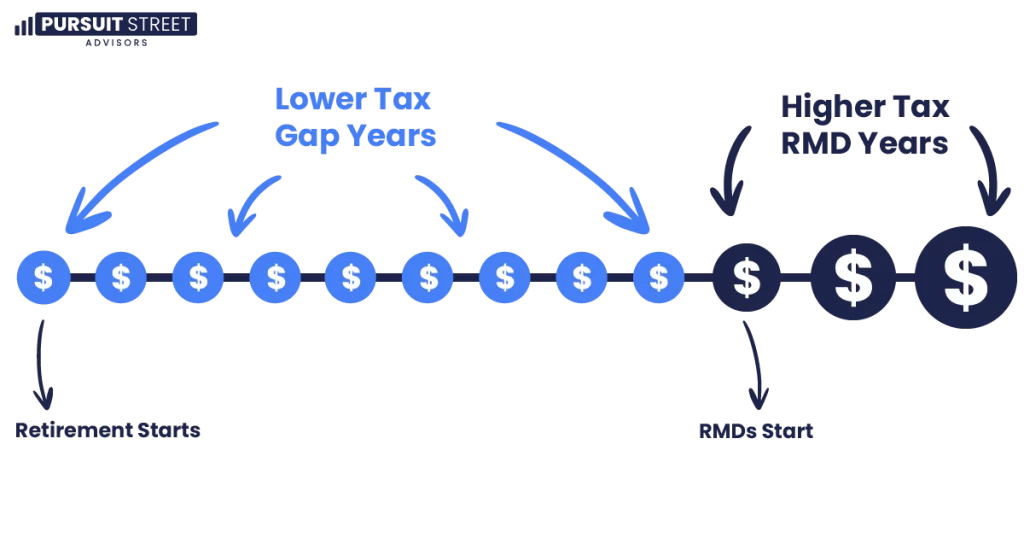

When you’re in school there is a term called a “gap year”.

It’s when you take time off from formal education in pursuit of travel, work, or volunteerism.

However, in retirement we can also take advantage of “gap years” – and it could save you tens or hundreds of thousands in lifetime taxes if you use them right.

These are the years between when you retire and when RMDs kick in at 73 (or 75 depending when you were born).

Think of it as your golden opportunity to slash your retirement tax bill.

Many retirees completely miss out on these opportunities, but savvy planners use them to dramatically reduce their lifetime tax burden.

Let me show you exactly how to do it….

#1. Time Your Social Security Like a Pro

Stop what you’re doing if you’re planning to take Social Security the moment you can.

Here’s what you need to know about the timing decision:

If your full retirement age is 67 and you elect to start benefits at age 62, the SSA will calculate your payments based on 60 months—a 20% reduction for the first 36 months and another 10% for the remaining 24 months, cutting your monthly Social Security benefits a total of 30%.

However, every year you wait between 67 and 70 adds 8% to your benefit – guaranteed.

That’s a guaranteed return you won’t find anywhere else in today’s market.

But the tax advantages are even bigger than the increased benefit.

By delaying Social Security, you create valuable space in lower tax brackets during your gap years.

This also delays the partial tax assessed on Social Security payments as well.

This space is like gold for tax planning. You can fill it with strategic Roth conversions, capital gains harvesting, and other tax-saving moves that could potentially save you thousands over the course of your retirement.

#2. Master the Roth Conversion Sweet Spot

As I mentioned above, during your gap years, you can partially convert traditional IRA money to a Roth IRA.

This is where the real tax magic happens.

Think about it: When you convert to a Roth during your gap years, you’re paying a little bit of tax each year at today’s rates, to avoid a lot of unknown taxes on big RMDs later.

Plus, all future growth is tax-free, and you’ll never face RMDs on the Roth money.

Through systematic Roth conversions you could save tens of thousands in lifetime taxes by converting to a Roth IRA annually during the gap years instead of facing massive RMDs at 73.

By partially converting a set amount annually and filling lower tax brackets allows you to convert at lower average rates across these years before any Social Security or RMDs begin and potentially move you into a higher tax bracket.

#3. Don’t Let Your Pension Block Your Strategy

Got a pension?

Timing is critical. Most pensions start paying at 65, creating taxable income that can block your Roth conversion opportunities.

This is where careful planning becomes crucial.

The fix?

Accelerate your Roth conversions before your pension kicks in.

If you have a pension starting at age 65 you could implement an aggressive Roth conversion strategy in the lower tax years before the pension, Social Security, and RMDs kick in creating additional taxable income.

#4. The Smart Way to Give to Charity

Love supporting causes you care about?

Here’s a tax-saving trick that most people miss entirely:

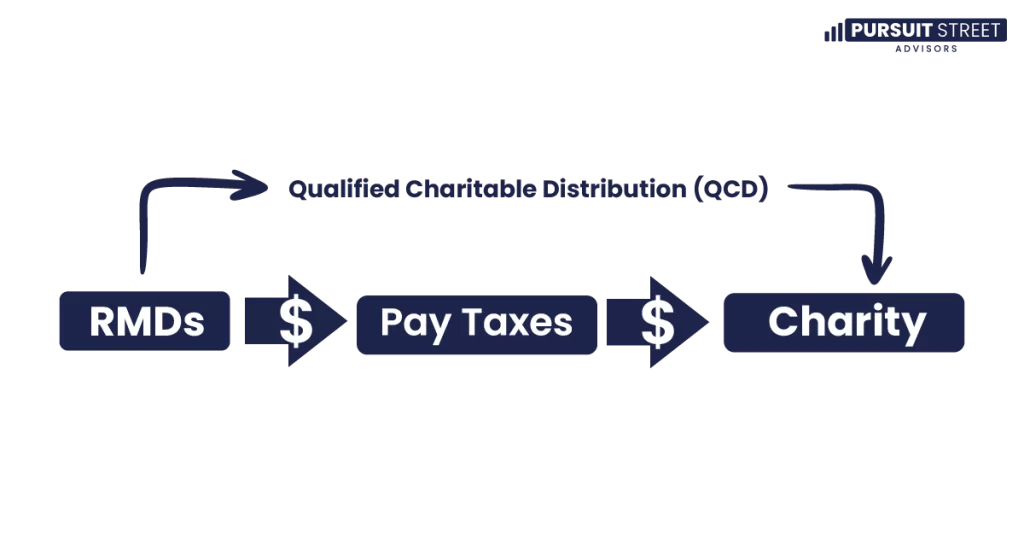

Instead of giving cash during your gap years, wait until 70½ and use Qualified Charitable Distributions (QCDs) to satisfy your RMDs.

If you waited to make a donation until age 73 (RMD age) – as opposed to age 62 – means money invested in an IRA will have an additional decade to grow.

This means that you may be able to donate more money, making a bigger impact for the charity receiving the donation and saving more money on taxes.

This strategy is powerful because:

-QCDs count toward your RMDs but don’t show up as taxable income

-You can give up to $100,000 annually this way

-It works even if you don’t itemize deductions.

For example, if you had planned to give $50,000 annually to your church. By waiting until age 73 and using QCDs, you could satisfy your RMD requirements and kept your taxable income lower, preserving other tax benefits.

If you are charitably inclined this is a possible reason to maintain a traditional retirement account balance and not convert all of your retirement accounts to Roth before RMDs start.

Another tax-efficient way to approach gifting is lumping charitable donations together.

Let’s walk through an example.

Say you’re donating $10,000 annually, and your other deductions total about $18,000 – putting you below the standard deduction threshold ($30,000 MFJ in 2025).

Following the traditional monthly giving approach over four years, you’d claim the standard deduction each time ($30,000 MFJ in 2025), totaling $120,000 in deductions.

But here’s where strategic timing comes into play.

Instead of spreading donations throughout the year, you can “bundle” them together. Here’s how it works:

First year: Hold onto your $10,000

Second year: Donate $20,000 (last year’s + this year’s contribution)

Third year: Hold onto your $10,000 again

Fourth year: Donate $20,000 (year 3 & 4 contributions)

This creates a powerful tax advantage:

Year 1: $30,000 (claim standard deduction)

Year 2: $38,000 (itemized – thanks to your larger charitable contribution)

Year 3: $30,000 (standard deduction, I assume this will be higher)

Year 4: $38,000 (itemized again)

The result?

Your total deductions jump to $136,000 – that’s $16,000 more than the traditional approach. For someone in the 24% tax bracket, this simple shift in timing could put almost $4,000 back in your pocket.

Best part? You’re still giving the same total amount to charity – just in a more tax-efficient way.

#5. Capital Gain Harvesting

Your gap years might put you in the lowest tax bracket you’ve seen in decades.

This creates a perfect opportunity to harvest capital gains – you might even pay zero federal taxes on long-term gains.

Current tax law allows married couples with taxable income under $96,700 (in 2025) to pay 0% on long-term capital gains. During your gap years, you might be able to:

– Sell appreciated stocks and pay no federal tax

– Reset your cost basis higher for future sales

– Diversify concentrated positions more tax-efficiently

For example, you could use your gap years to sell $100,000 of highly appreciated stock you’ve held for 20 years.

Your total tax bill on these sales? Zero after factoring in the standard deduction.

Had you waited until pension, Social Security or RMDs started it would have created additional taxable income and you could have paid thousands more in capital gains taxes.

#6. The Working Retirement Loophole

Still working past 73?

Many people are working well into their 70’s with the many advancements in modern healthcare.

Which means…

#1 You’ll likely want to delay Social Security. If you are working, delaying Social Security makes extra sense. This is because you’ll already have income – and taxes – from working. However after age 70 there is no additional benefit to postponing Social Security beyond tax purposes.

#2 You might be able to delay RMDs from your current employer’s retirement plan.

This could again save working folks thousands in unnecessary taxes.

Key requirements for this strategy:

– Must not own more than 5% of the company

– Plan must allow for this delay

– Only works for current employer’s plan

For someone with $1 million in retirement accounts, proper gap year planning could save tens of thousands in lifetime taxes. The savings can be even more dramatic for larger accounts.

But here’s the catch – and it’s a big one:

You need to start planning years before retirement. Wait until you’re 73, and you’ve missed the boat entirely.

The key is to:

– Start planning at least 5-10 years before retirement

– Create a year-by-year tax projection

– Coordinate all of your income sources

– Monitor tax law changes and adjust accordingly

If retirement is within 10 years, here’s your step-by-step plan:

The government created rules that can force you to pay massive taxes in retirement.

But they also created opportunities to legally avoid many of these taxes – if you know where to look and plan ahead.

Your retirement savings took decades to build.

Don’t let poor tax planning take a huge bite out of them.

The gap years strategy could be your biggest opportunity to keep more of your hard-earned money where it belongs – in your pocket.